As Mexico and Saudi Arabia fight over a deal to bring the oil-price war to an end, Mexico has a powerful defense: a massive Wall Street hedge shielding it from low prices.

With talks well into their third day, the Mexican sovereign oil hedge, which insures the Latin American country against low prices and is considered a state secret, is a factor that may make the country less inclined to accept the OPEC+ agreement.

For the last two decades, Mexico has bought so-called Asian style put options from a small group of investment banks and oil companies, in what’s considered Wall Street’s largest — and most closely guarded — annual oil deal.

The options give Mexico the right to sell its oil at a predetermined price. They are the equivalent of an insurance policy: the country banks all gains from higher prices but enjoys the security of a minimum floor. So if oil prices remain weak or plunge even further, Mexico will still book higher prices.

The hedge isn’t the only reason Mexico is holding out. But it strengthens the country’s hand and makes it less desperate for a deal than countries whose budgets have been ravaged by the collapse in oil prices since the start of the year — first because of the coronavirus and then because of the price war launched by Saudi Arabia.

The main reason driving President Andres Manuel Lopez Obrador, a left-wing populist, to resist the deal is his pledge to revive oil production via state-owned Petroleos Mexicanos. Slashing 400,000 barrels a day to comply with the OPEC+ deal, rather than the 100,000 barrels a day that Mexico has counter-offered to Saudi Arabia, would put on hold his ambitious plan to return Pemex to its former glory.

The hedge has shielded Mexico in every downturn over the last 20 years: it made $5.1 billion when prices crashed in 2009 during the global financial crisis, and it received $6.4 billion in 2015 and another $2.7 billion in 2016 after Saudi Arabia waged another price war.

The operation comes at a cost. In recent years, Mexico has spent about $1 billion annually buying the options.

“The insurance policy isn’t cheap,” Mexican Finance Minister Arturo Herrera told broadcaster Televisa on March 10. “But it’s insurance for times like now. Our fiscal budget isn’t going to be hit.”

Pemex, the state-owned company, has its own separate, smaller oil hedge. This year, Pemex hedged 234,000 barrels a day at an average of $49 a barrel.

State Secret

Mexico has disclosed very few details about its insurance for 2020 after it declared the sovereign hedge a state secret. However, based on limited public information, alongside historical data about previous years, it’s possible to make a rough estimate of the potential payout if prices remain low.

The government told lawmakers it has guaranteed revenues to support the assumptions for oil prices made in the country’s budget — of $49 a barrel for the Mexican oil export basket, equivalent to about $60-$65 a barrel for Brent crude.

It locks in that revenue via two elements: the hedge, and the country’s oil stabilization fund. The fund historically has only provided $2-$5 a barrel, so it’s realistic to assume that Mexico hedged at $45 a barrel at least for its crude. In the past, Mexico has hedged around 250 million barrels, equal to nearly all its net oil exports in an operation that runs from Dec. 1 to Nov. 30.

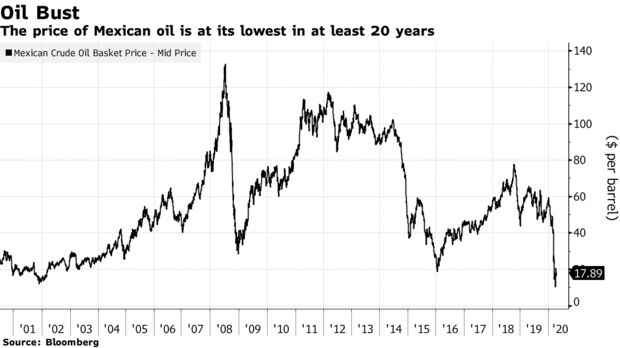

Using all those elements, a rough calculation suggests that if the Mexican oil export basket were to remain at current levels, the country would receive a multi-billion-dollar payout. Since December, the Mexican oil basket has averaged $42 a barrel.

If current low prices for Mexican oil continue until the end of November, the average would drop to just above $20 a barrel, and the hedge would pay out close to $6 billion, according to Bloomberg News calculations.

Representatives of the Finance Ministry and Energy Ministry declined to comment.

Saudi says Mexico needs to join OPEC deal

Saudi Arabia’s energy minister said on Friday that a final OPEC+ oil supply pact to reduce 10 million barrels per day (bpd), which was agreed on Thursday, hinges on Mexico joining in the cuts.

OPEC, Russia and other allies, a group known as OPEC+, outlined plans on Thursday to cut their oil output by more than a fifth but said a final agreement was dependent on Mexico signing up to the pact after it balked at the production cuts it was asked to make. Discussions among top global energy ministers will resume on Friday.

“I hope (Mexico) comes to see the benefit of this agreement not only for Mexico but for the whole world. This whole agreement is hinging on Mexico agreeing to it,” Prince Abdulaziz bin Salman told Reuters by telephone.

Global fuel demand has plunged by around 30 million bpd, or 30% of global supplies, as steps to fight the coronavirus have grounded planes, cut vehicle usage and curbed economic activity.

The kingdom will host an extraordinary meeting by video conference at 12.00 GMT on Friday for energy ministers from the Group of 20 major economies.

Asked about other countries such as the United States, Canada and Brazil joining the OPEC+ cut pact, Prince Abdulaziz said: “They will do it in their own way, using their own approaches, and it is not our job to dictate to others what they could do based on their national circumstances.”

He added that he expects that other producers will join in the global effort to reduce oil supply to stabilise oil markets.

The planned output curbs by OPEC+ amount to 10 million bpd, or 10% of global supplies, with another 5 million bpd expected to come from other nations, according to sources, to help deal with the deepest oil crisis in decades.

The agreement will take about 11.3 million bpd of actual crude supply from the market “provided that Mexico agrees”, Prince Abdulaziz said.

Saudi Arabia has agreed a lower baseline for its production cut than its April output which is about 12.3 million bpd, making the kingdom’s effective share of reduction at about 3.8 million bpd.

Source: .bloomberg.com, reuters .com

The Mazatlan Post